Thrift Savings Plan Basics

TSP 101

What is the TSP?

The Thrift Savings Plan (TSP) is the Federal Government and Military Service version of a 401k plan. It is a Defined Contribution plan where employees can contribute a percentage of their pay, on a tax deferred basis, and the government will match those contributions up to 5%. You can establish either a Traditional TSP account or a Roth TSP account. If you have a 401k from a past employer, you can roll that into your TSP account (restrictions apply). Expanded withdrawal options allow retirees to withdraw from TSP in almost any way they choose. In the end, the TSP is a wealth building vehicle designed to supplement your pension and Social Security payments in retirement. Your ability to grow your TSP account can have a very big impact on your overall financial picture in retirement!TSP Fund Options

The simplicity of TSP is both a blessing and a curse! With only 5 core TSP fund options, investing in the TSP is very simple. There are 3 stock index funds, 1 bond index fund, and a special kind of money market fund. You can mix and match within the 5 funds or utilize the L funds which do the fund allocation for you based on your expected retirement date.

The C fund tracks the S&P500 index. The ticker symbol for the index is $SPX or SPY as the exchange traded fund (ETF)

The S fund tracks the Dow Jones U.S. Completion Total Stock Market Index. The ticker symbol for the index is $DWCPF or VXF as the ETF.

The I fund tracks the Europe, Australasia, Far East Index. The ticker symbol for both the index and the ETF is EFA.

The F fund tracks the Bloomberg Barclays U.S. Aggregate Bond Index. The ticker symbol for the index and ETF is AGG.

You can put these ticker symbols into any charting app or website to create a price chart of the corresponding TSP fund.

The G fund is a special type of Money Market fund created solely for TSP investors. There is no ticker symbol. The rate of return is tied directly to the FED Funds Rate. When interest rates are coming down, the rate of return for the G fund is declining. When interest rates are moving up, the rate of return of the G fund is also moving up. Most importantly, the G fund cannot have a negative quarter by statute. You can never lose your principle when invested in the G fund.

The L funds do not have ticker symbols. They are combinations of the 5 core TSP funds, reallocating quarterly to decrease exposure to the stock funds as you progress along in your career. The objective is to decrease risk exposure to the stock funds as you get closer to retirement.

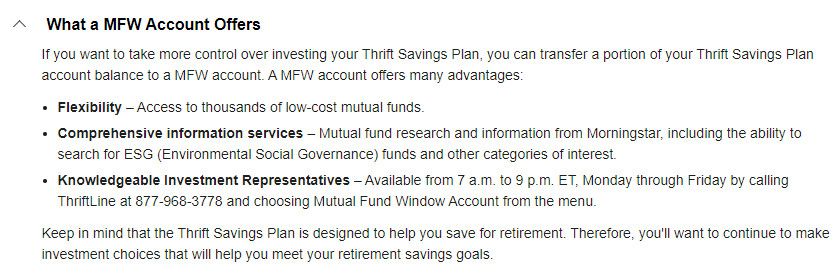

The Mutual Fund Window (MFW) is an option added to the TSP fund line-up in 2022. The MFW enables TSP investors to transfer up to 25% of the amount of their TSP account into a separate, self-directed Mutual Fund account. The MFW gives TSP investors access to 5,000 +/- mutual funds encompassing virtually every possible asset class. The MFW is completely separate from core TSP and is not governed by the TSP rules for reallocation. Restrictions and fees apply.

TSP.gov

Virtually everything you do with respect to TSP happens on the TSP.gov website but, there are several important exceptions. First, your agency's HR department must opt you in to TSP initially. Second, if you want to change the amount that you contribute to TSP each payday, that is also handled by your HR department. Every other function related to TSP can be accessed at TSP.gov or by calling the TSP help desk at 1-877-968-3778.

Changing Investments

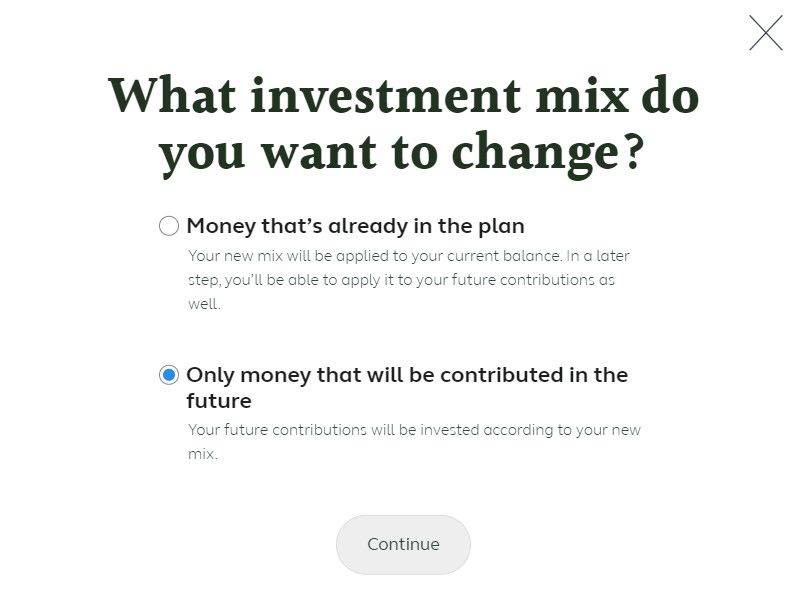

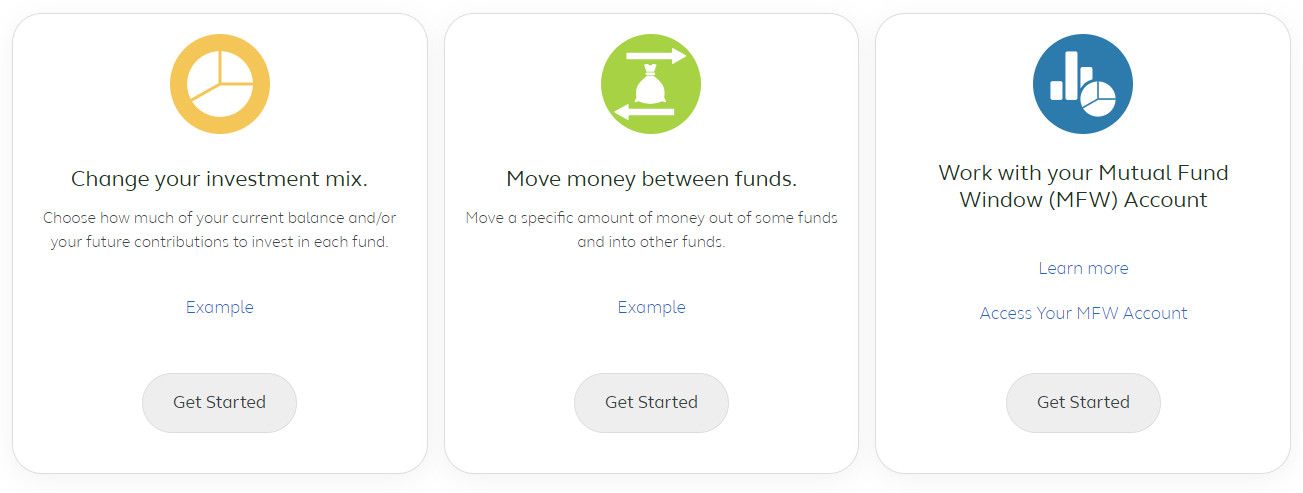

There are 2 buckets of money associated with your TSP account. The first is the new money that you contribute to TSP each payday. This bucket is relatively fixed. It only changes when you change the amount you contribute. If you want to change the funds to which your new money is going, you click the Change Your Investment Mix tab and select Future Contributions Only.

* There is NO LIMIT to the number of times you can switch funds for FUTURE contributions *

To change the funds in which your core account is invested, you have two options. You can use the Change Investment Mix option or the Move Money Between Funds option.

* The TSP restricts the number of times you can reallocate between the funds in your core account *

The 2 Move Per Month Rule

There are 2 critically important rules to understand when actively managing your TSP account. The first is the "2 Move per Month Rule". While this seems very straight forward, the application of this rule can be tricky...

Each calendar month you get two unlimited moves between the core TSP funds. You can change the % invested between any of the 5 core funds and the L funds. After the second move in a calendar month, any additional move can only increase your holding in the G fund. From a tactical perspective, if you use your 2 moves early in the month, your options to maximize any market gains later in the month are extremely limited. We go into great detail describing the application of this rule, with examples, in the e-book. It's a MUST READ!

The Noon Rule

While we can track the indexes to which the core TSP funds are associated on a minute to minute basis, the TSP funds themselves are calculated after the market closes each night. If you submit request to reallocate funds before 1200 PM East Coast Time, you will get that day's closing price. If your request is made after 1200PM East Coast Time, you will get the next trading day's closing price. This can be extremely confusing! Again, we go into great detail, with examples, in the e-book.

Understanding your 2 buckets of money, and the restrictions that apply to each, is CRITICAL to effectively maximize your TSP account!

Mutual Fund Window

The Mutual Fund Window (MFW) is a self-directed account option for TSP investors. The MFW is provided by a third party and is not subject to the restrictions of the core TSP funds. There are several fees associated, along with other restrictions. The MFW is designed for TSP investors who desire investment access to specific asset classes or segments that are not available in core TSP. The MFW can be used in many different ways to support or augment your core TSP account. Financial advisors are available to assist in working through option. Contact them at the number below.

Bottom Line

The TSP basics are relatively straight forward. You need to understand the function of the TSP and how it fits into your overall retirement picture. You need to make some decisions about your contribution amounts and how those contributions will be allocated. Most importantly, you need to have your TSP.gov username and password readily available to actively manage your account; being in the stock funds when the market is trending up, and protecting those gains when the market is trending down.