Passive vs. Active TSP Investment Strategies

What kind of investor are you?

There are only 2 kinds of TSP investment Strategies, Passive and Active. The TSP can be a very big piece of your overall retirement plan but, it doesn’t happen on its own. Most people understand this but don’t have the time or interest needed to really maximize their TSP. Determining what type of investor you are is another soul searching, but very valuable, exercise. Do your eyes roll to the back of your head thinking about finances, retirement and stock charts? You’re most likely a Passive Investor. If you get excited about maxing out your TSP account and retiring as a “TSP Millionaire”, then you’re most likely an Active Investor.

Passive Investing in the TSP

Passive investing includes strategies like the L Funds, “Buy & Hold”, “Set it and Forget it”, the “70/30 Method”, etc… These methodologies are generally the Conventional Wisdom of TSP investing.

The core of Passive Investing is to pick a strategy that fits your personal risk tolerance and stick with it thru the market ups and downs. Passive investing is based on YOU. Your risk tolerance, your level of financial intelligence, proximity to retirement, your financial goals, your ability to sleep well at night, etc… It’s also based on your BELIEF in the conventional wisdom of retail retirement investing; “The market always goes up over time”. IF the market always goes up then you can ride the ups and downs with little concern, as you will certainly come out ahead in the end. Unfortunately, there is no certainty in investing and the market does NOT always go up. Also, riding those ups and downs goes against our most important rule…don’t lose money.

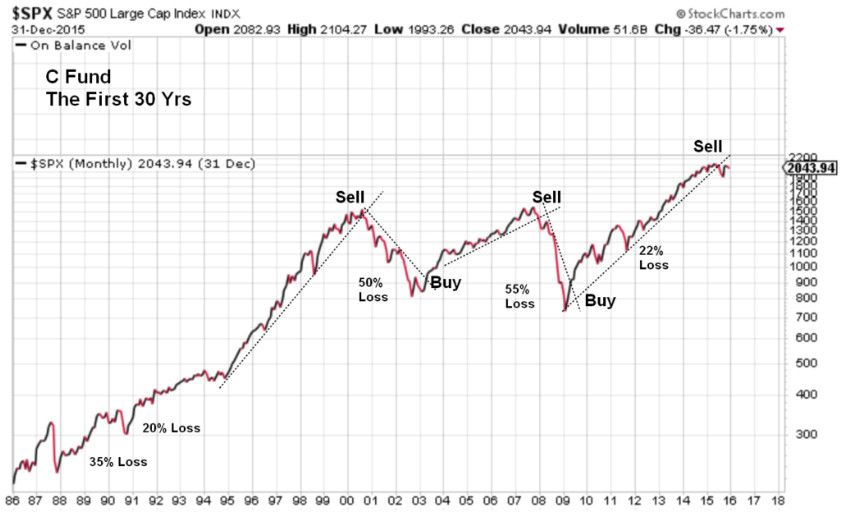

The TSP was established in 1986. Below is a chart of the S&P500 (C Fund) over the first 30 years of its existence. Did the market go up over time? Absolutely! The C fund increased in value 10-fold over those first 30 years! Along the way, however, passive investors had to stomach at least five instances of 20+% losses; including two 50% losses!

Depending on where you were relative to retirement, these periods of loss could have been devastating. This is the problem with Passive Investing. It is based on linear, historical math that can be gut wrenching in real-time.

L Funds

Conventional Wisdom says that the Market always goes up. Conventional wisdom also says that you should be less “risky” as you progress along in your career. Along comes the L Funds to meet the need. The L funds are a passive approach to TSP investing that automatically decrease your exposure to the TSP stock funds each quarter over the course of your career.

You simply select the L fund that is closest to your projected date of retirement (or the date that you expect to begin withdrawals), max out contributions to that fund throughout your career, and don’t look at it again until you’re about to retire. What’s so enticing about the L funds is their ease of use, conformity to the conventional wisdom, and hands-off approach. The individual TSP investor just needs to pick a date in the future and the L fund algorithm does the rest. But, does the market care about their algorithm?

Buy & Hold

This strategy is exactly what the name implies. The individual investor picks a fund, using any criteria they choose, and keeps buying that fund throughout their career. As the price of the fund goes up and down, the investor is buying greater or fewer shares, based on the fixed contribution amount. This way, you are accumulating more shares when the price is relatively low and fewer shares when the price is relatively high. In this way, you would maximize the number of shares purchased for the dollar amount invested over time. However, as your core account grows, the price fluctuation of your selected fund affects its value. The magic of Compounding works in both directions.

Set it & Forget It

This strategy is even less active than Buy & Hold. Buy & Hold investors may periodically research which funds are out-performing and adjust their allocation accordingly. Set It and Forget It investors simply pick a fund, set the process in motion and hope for the best in the end.

The “70/30 Method” is a version of “Set It and Forget It” that was made famous by Warren Buffett. The method consists of setting your allocation to 70% C fund, 30% G fund and leaving it alone until you retire. The idea is that when the market is trending up, the investor is enjoying 70% of the gains. When the market is trending down, the investor is only exposed to 70% of the downside risk. Another version of this method is 70% C fund and 30% F fund. While there is some risk associated with the F fund, the idea is that bonds tend to do better when stocks are decreasing in value.

All the methods above, and their assorted variations, provide a convenient and hands-off approach to TSP investing. They require very little work on the part of the investor, and they are in line with conventional investing norms.

What you DON’T see in any of these passive methods is a goal of Maximizing your TSP account.

The Pros & Cons of Passive Investing in the TSP

Pros

It's convenient.

It's so easy "even a Caveman could do it."

There is no need for you, the TSP account holder, to invest much time or effort.

Going along with the Conventional Wisdom makes us feel good, regardless of the end result.

Cons

The focus is on convenience and ease use, not the end result.

Major market fluctuations are not taken into account.

Risk is based on your personal circumstances and tolerance, not on the Market.

Active Investing in the TSP

The alternative to Passive Investing is Active Investing. Where passive investing is based on you, the individual, active investing is primarily based on the Market. Active investors utilize the analysis of price (technical analysis) along with indicators, trend lines, and pattern recognition.

The goal is to identify changes in market trend as early as possible. By identifying these changes early, active investors can be fully allocated in the TSP funds when the market is trending up and manage downside risk, using the G and F funds, when the market is trending down.

Below is the same chart of the first 30 years of the C fund, showing simple trend line analysis of major trend changes during this time period. Utilizing this one technique, would active investors have avoided all losses? Would they have reallocated at the top and bottom of each trend change? Of course not! BUT, they would have enjoyed the majority of market gains and avoided the majority of market losses.

The Myth of “Market Timing”

We’ve all heard people say, “You can’t time the market!”. The conventional wisdom beats this into us with a hammer! What is Market Timing? Investopedia defines market timing as “… the act of moving investment money in or out of a financial market or switching funds between asset classes based on predictive methods. It is often a key component of actively managed investment strategies and is almost always the basic strategy for traders. Predictive methods for guiding market timing decisions may include fundamental, technical, quantitative, or economic data.”

The idea of Market Timing is in utilizing analytical methods to PREDICT the direction of the market. Prediction implies a Crystal Ball. If the prediction does not materialize as expected, the analyst and methodology are written off. The Conventional Wisdom can be so ingrained that even successful Market Timers are often written off as lucky at best or deceptive at worst.

Market timing is a valid investment strategy. It can be used in conjunction with Technical and Fundamental Analysis to produce incredible returns. BUT, given the restrictions of the TSP reallocation rules, Market Timing is NOT a useful strategy for TSP investors.

Technical Analysis

Investopedia defines Technical Analysis as, “Technical analysis is a trading discipline employed to evaluate investments and identify trading opportunities by analyzing statistical trends gathered from trading activity, such as price movement and volume.

Unlike fundamental analysis, which attempts to evaluate a security’s value based on business results such as sales and earnings, technical analysis focuses on the study of price and volume. Technical analysis tools are used to scrutinize the ways supply and demand for a security will affect changes in price, volume and implied volatility. Technical analysis is often used to generate short-term trading signals from various charting tools but can also help improve the evaluation of a security’s strength or weakness relative to the broader market or one of its sectors. This information helps analysts improve their overall valuation estimate.”

Fundamental Analysis

Investopedia defines Fundamental Analysis as, “Fundamental analysis (FA) is a method of measuring a security’s intrinsic value by examining related economic and financial factors. Fundamental analysts study anything that can affect the security’s value, from macroeconomic factors such as the state of the economy and industry conditions to microeconomic factors like the effectiveness of the company’s management. The end goal is to arrive at a number that an investor can compare with a security’s current price in order to see whether the security is undervalued or overvalued.

This method of stock analysis is considered to be in contrast to technical analysis, which forecasts the direction of prices through an analysis of historical market data such as price and volume.”

Seasonality Trading

Seasonality trading is a version of active trading based on price volatility during a given time of the year. StockCharts.com describes Seasonality as follows:

“Seasonality is the tendency for securities to perform better during some time periods and worse during others. These periods can be days of the week, months of the year, six-month stretches or even multi-year timeframes. For example, Yale Hirsh of the Stock Traders Almanac discovered the six-month seasonal pattern or cycle. Since 1950, the best six-month period for the S&P 500 extends from November to April. By extension, the worst six-month period runs from May to October, which is where the phrase “sell in May and go away” comes from. StockCharts.com offers a seasonality tool that chartists can use to identify monthly seasonal patterns. This article will explain how this tool works and show what chartists should look for when using our Seasonality Charts."

What sets Active Investing apart from Passive Investing is the focus on the Market movement vs the individual investor. As an active investor, whether you are utilizing Technical Analysis, Fundamental Analysis, Seasonality, or a combination, your goal is to maximize gains and minimize downside risk based on Market movement.

The Pros & Cons of Active Investing in the TSP

Pros

- You take responsibility for your Rate of Return.

- Your performance depends on your ability to apply the tools.

- You take Hope, Fear, and Greed out of the equation

Cons

- You have to put in the work.

- You have to make difficult decisions.

- You have to fight conventional wisdom.

To understand the Grow My TSP methodology and how we use it as a TSP investment strategy, make sure to review the Our Strategy page.