TSP Lifecycle Funds - Pros & Cons

The TSP recently launched the L2075 Fund. According to TSP.gov, the fund is designed for federal employees or military service members who were born after 2009 or those expecting to withdraw from TSP beginning in 2073 or later. The fund is looking 50 years into the future! This post will use the new L2075 fund as an example to explain how the Lifecycle Funds work, their pros and cons, and whether or not they work for your investment personality.

The L2075 Investment Objective

Below is the fund objective directly from TSP.gov. The objective is to "achieve a high level of growth with a very low emphasis on preservation of assets". TSP investors considering this fund should consider both aspects of the statement; high growth AND very low emphasis on preservation of assets.

How Do The L Funds Work?

The L funds are a "set it and forget it" approach to TSP investing where the fund does all the work.

"The L 2075 Fund was designed by investment professionals to offer a diversified mix of the five individual TSP funds (G, F, C, S, and I). Its goal is to provide the best expected return for the amount of expected risk that is appropriate for its investors. Its target asset allocation is based on assumptions about future returns, inflation, economic growth, and interest rates. Each day, the assets in the L 2075 Fund are rebalanced across the five individual funds to maintain the allocation targets. Over time, those targets change automatically to become more conservative — meaning the fund will hold less of the C, S, and I Funds and more of the G and F Funds." - TSP.gov

There are three main components of the L funds that align with the statement above.

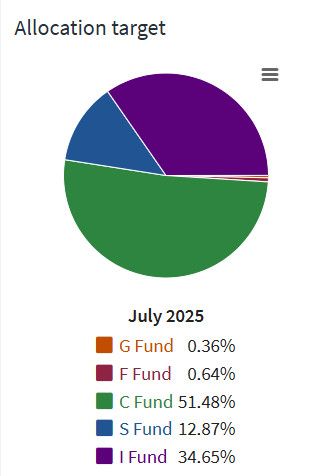

The first is focused on the mix. The L funds are a combination of the 5 core TSP funds. Each L fund is designed by professional fund managers (Blackrock) who determine how much of each core TSP fund goes into the specific L fund. The determination is based on assumptions of future returns, inflation, economic growth, and interest rates. This happens at the inception of each new L fund and is revisited approximately every 5 years throughout the life of the fund. The result is the Target Allocation. For the L2075 fund, the target allocation is below.

The second component is Daily Rebalancing. At the close of every trading day, the fund automatically rebalances to align with the allocation target.

Let's say that the C fund goes up 2% today and the I fund goes down 2%. That would result in the C fund being over allocated, and the I fund under allocated, based on the target. The fund would automatically sell shares of the C fund and buy shares of the I fund to bring the overall target allocation back into balance based on the defined percentages.

This type of rebalancing can be viewed in two ways. First, it could be considered dollar cost averaging. The fund is buying shares in the components that are down the most that day, therefore buying relatively more shares. The second way to view rebalancing is that the fund is selling its winners, which are likely to continue higher, and buying its losers, which are likely to continue lower.

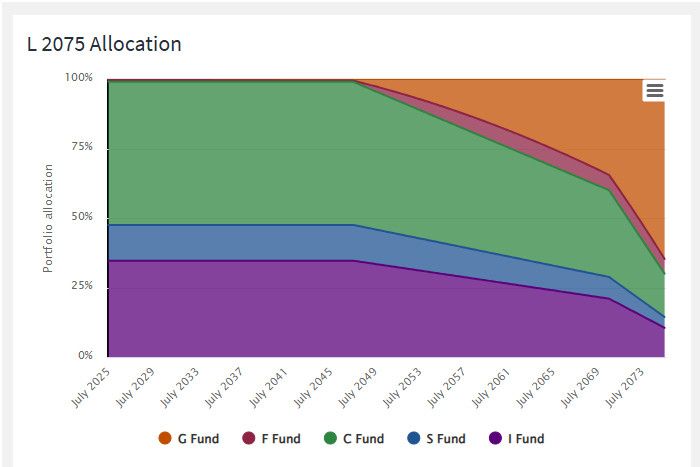

The third component is that the allocation targets change every quarter, automatically decreasing fund exposure to the stock funds and increasing exposure to the F and G funds. Quarterly changes to the target allocations are based on the concept that stocks are inherently more risky than bonds. Each L fund reduces its exposure to riskier stock funds and increases its exposure to bonds incrementally over the life of the fund. This does not happen linearly.

As the chart below shows, TSP investors in the L2075 fund will be predominantly invested in the stock funds from 2025 to 2048. At that point, the target allocations begin to change materially, out of the stock funds and into the less risky F and G funds.- TSP.gov

Pros & Cons

The L funds can be a great choice for government employees and military service members who want a "set it and forget it" investment strategy. While this level of convenience is certainly a factor to consider, there are also downsides to the L funds. Below are the major pros and cons.

Pros of L Funds

Simplicity – No need to manage allocations yourself; one fund provides diversification.

Automatic Rebalancing – The fund regularly rebalances to stay aligned with its allocation targets.

Glide Path to Retirement – Reduces risk automatically as you approach retirement age.

Diversification – Exposure to all five individual TSP funds, spreading risk across asset classes.

“Set It and Forget It” – Ideal for those who don’t want to monitor the market or adjust allocations.

Cons of L Funds

One-Size-Fits-All – Glide paths are designed for the “average” investor, not your personal risk tolerance or circumstances.

Less Flexibility – You can’t overweight certain funds (e.g., more C Fund or less I Fund) if you believe they’ll outperform.

Overly Conservative Near Retirement – As you approach your retirement date, L Funds become heavily weighted in G and F Funds, which may limit long-term growth if you’re planning for a lengthy retirement.

No Control Over Timing – You might miss opportunities to take advantage of market conditions or manage risks more actively.

Hidden Complexity – While simple on the surface, the fund’s internal allocation changes over time, which some investors may not fully understand.

Are The L Funds Right For You?

There is no one size fits all answer to this question. We all have different circumstances, risk tolerance, interest in investing, etc.

If you are looking for an easy "set it and forget it" type of investment strategy, the L funds may be a perfect fit. If you are more engaged in your investments, with the goal of maximizing gains while minimizing downside risk, the L funds may not be the best choice.

Fortunately, you are not stuck with your choice. As circumstances change throughout your career, you are free to change your investment strategy. Early career investors may opt for the L funds as they are focused on work, family, promotions, etc. Later career employees and retirees may have more time to dedicate to their investments and have less tolerance for downside risk.

Understanding the goal of the L funds and how they work is the first step toward making the best TSP investment decision for you and your family.

-----------------------------------------

GrowMyTSP.com does not provide personal investment advice. We are an education and analysis service, helping TSP investors grow their accounts using strategies and models that best fit their personal circumstances and risk tolerance. Get started at GrowMyTSP.com.