Factors that affect TSP account growth

There are only 3 factors that affect the growth of your TSP account:

- Contribution

- Time

- Rate of Return

Contribution:

You can contribute up to the IRS annual limit. The government contributes an automatic 1%, matches your contribution for the first 3%, then matches ½ on the next 2%. In total, if you contribute 5% of your pay to TSP each payday, the government matches that 5%.

It can be difficult to carve out dollars to invest in TSP, especially early in your career. However, you NEED to contribute a MINIMUM of 5%. With the government’s matching, you just made a 100% return on your 5% investment. It’s a NO BRAINER!

Beyond that, invest as much as your circumstances allow. As your salary increases your contributions should also increase. Aim to get your contribution to the IRS maximum as quickly as possible.

The dollars you contribute, along with the government’s matching, will be used to buy shares of the TSP funds. As the market moves up and down, your contribution each payday buys more or fewer shares depending on their price.

When prices are low, you are buying more shares; when prices are higher, you are buying fewer shares. This is known as Dollar Cost Averaging (DCA).

Because TSP investors contribute a fixed amount at fixed times each month, DCA occurs automatically. While an important component with respect to contributions, the value of DCA decreases as your overall TSP account grows.

Time (The Magic of Compounding):

As a new federal employee, the growth of your account is affected mostly by the amount you contribute. As time goes by, the magic of compounding takes over and enables your account to grow exponentially!

Compounding refers to how the value of your account increases over time. For instance, let’s say your contributions are all going to one fund. If you have $100 in your account and that fund increases by 1%, you will then have $101. If that fund increases another 1% the following day, you will then have $102.01.

As time goes by and the fund’s price continues to climb, the value of your account will continue compounding!

This effect constitutes the most important factor in the long-term growth of your TSP account.

The more you contribute, and the more time you allow compounding to work its magic, the larger your TSP account will be at retirement.

Over time, the compounding effect of your base account and how it’s allocated will be much more important than the amount you contribute each payday.

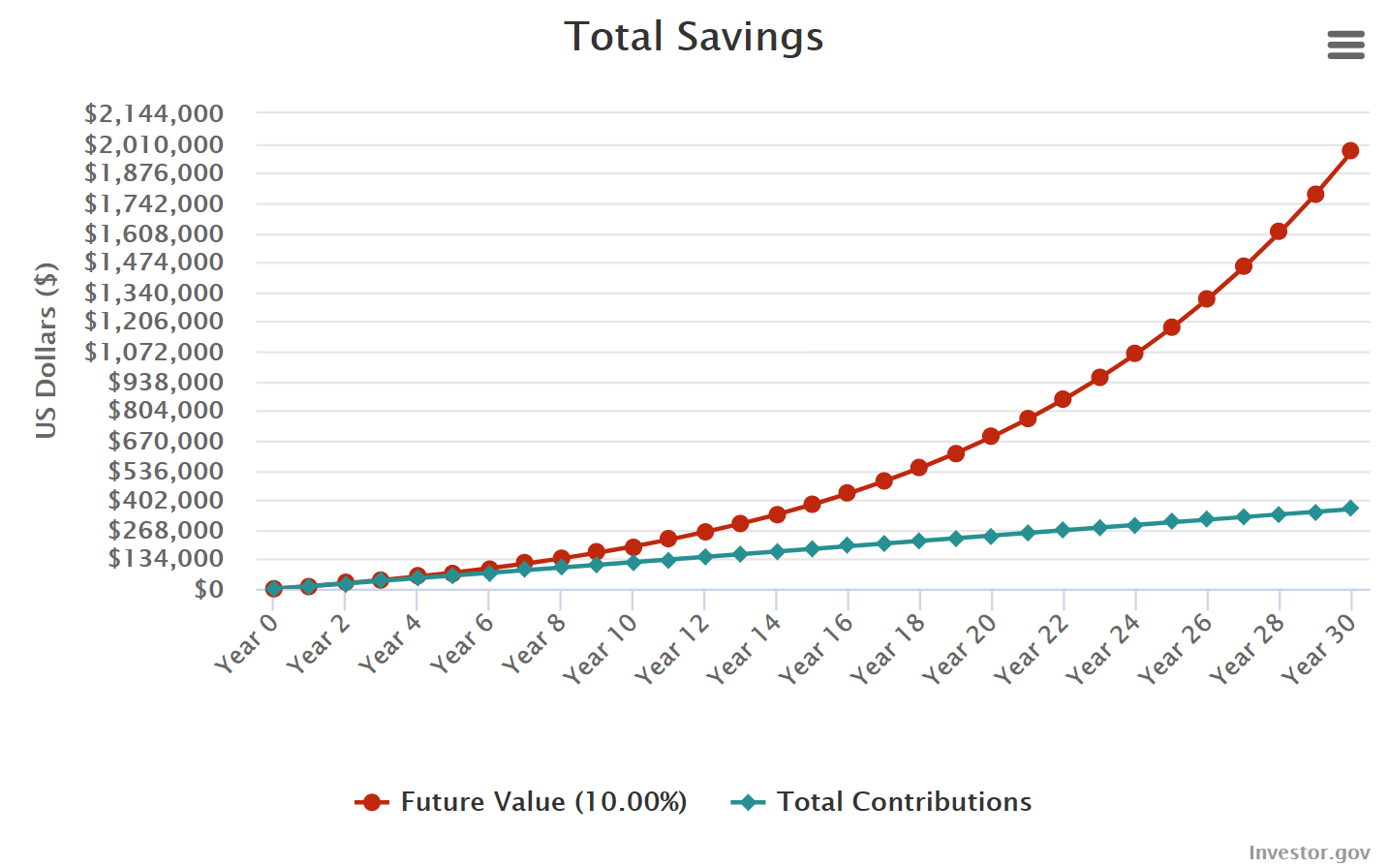

The chart below shows a $1,000 investment per month for 30 years, with a fixed rate of return of 10%.

In the first 5 years, the value of the account is mostly made up of contributed funds. But by year 12, the importance of compounding becomes clear.

Over time, the value of the account increases exponentially even though monthly contributions remain consistent.

Compounding Chart:

Rate of Return:

The third factor affecting the growth of your TSP account is the rate of return (ROR) that you can achieve over your career. While the chart above assumes a 10% fixed rate of return per year over 30 years, our reality includes good years and bad years.

If your account is allocated between the TSP funds that increase the most (or decrease the least) over time, you will maximize the rate of return of your TSP account. This seemingly simple statement is crucial to understand!

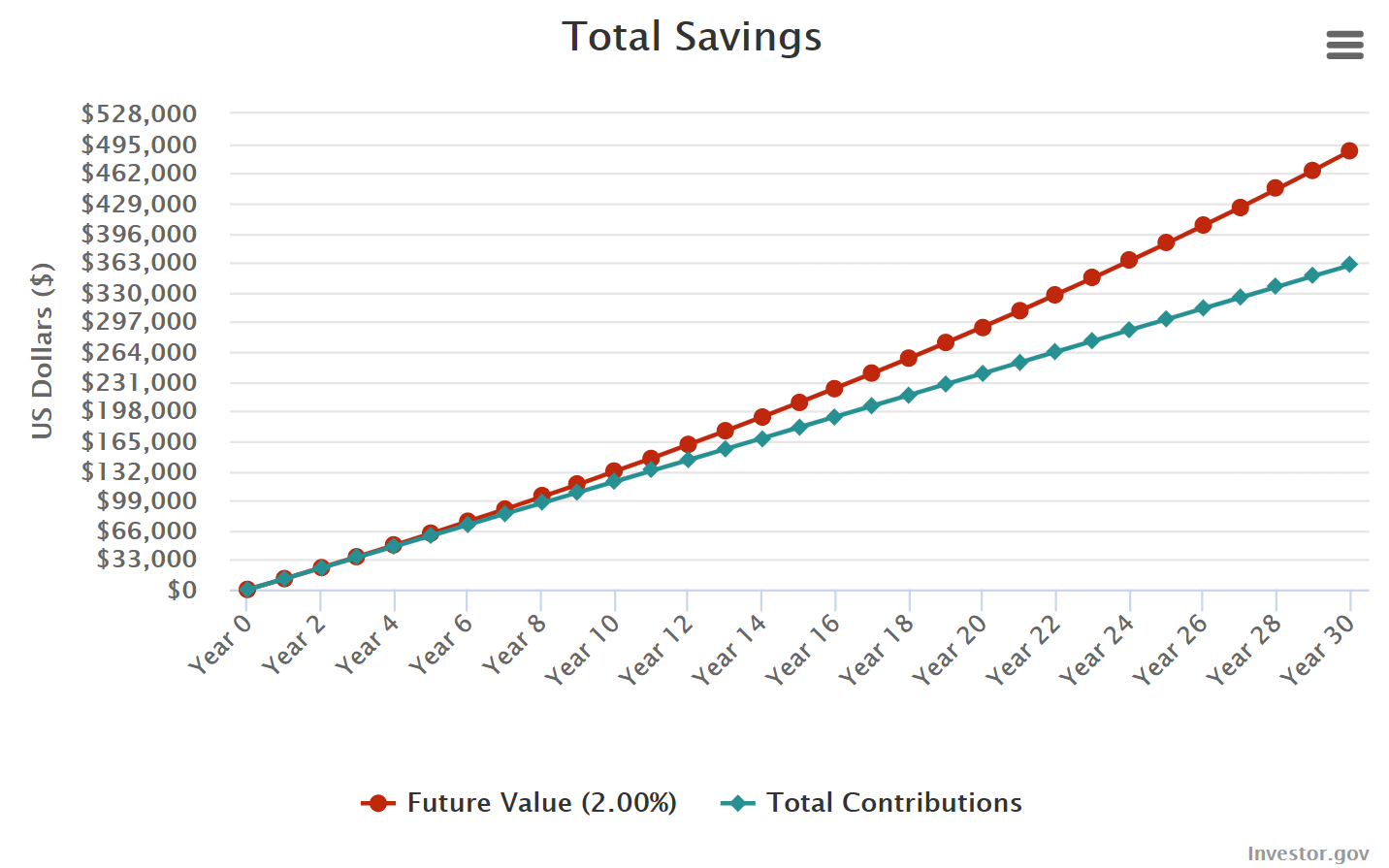

If you are a very conservative TSP investor with your allocation at 100% G fund, then your ROR will be consistent but meager as illustrated in the chart below.

Compounding Chart (G Fund):

If you are a riskier TSP investor, always allocated in the TSP stock funds, then you will see big gains AND big losses in the value of your account over time.

If you were fully allocated in the C fund over the past 30 years, the value of your account would look much more volatile as the chart below shows.

C Fund past 30 years:

These 3 factors directly impact the growth of your TSP account: Contribution, Time, & Rate of Return.

The amount you contribute each payday is relatively fixed. It can grow as you increase your contribution amount but caps out at the IRS maximum.

The amount of time you have for compounding to do its magic is also mostly fixed. The sooner you start investing in TSP, the more you will have in retirement; it’s that simple.

Maximizing your ROR is largely within your control, IF you choose it.

Your ROR will be based on the market ups and downs over the course of your career, and your ability to navigate those ups and downs...

The question is...how active a role are you willing to take in managing your TSP?

In the next lesson we will discuss which investing related factors affect YOU personally, as opposed to just affecting your TSP account.

Click the "Return to course" button below and then select your next lesson...see ya there!

Explore more courses