F Fund or G Fund During A Major Market Correction

During a major stock market decline, TSP investors have a choice. First, we can ride out the decline in anticipation of the eventual recovery. Second, we can reallocate out of the falling stock funds into the safety of the bond funds; G and F funds. While many TSP investors will opt to ride out the decline, retirees or more active investors may choose to reallocate out of falling stock funds to preserve their current account value. For those who choose the latter option, the question becomes, is the G or F fund a better option during a falling stock market.

While both the G and F funds are bond funds, there is a very big difference between the two.

The Case For The G Fund

According to the law establishing the TSP, the G Fund is technically called the "Government Securities Investment Fund,” and it invests in “special interest-bearing obligations of the United States" issued by the Treasury Department. Because Treasury issues the “special” “obligations” directly to the fund, they are not tradeable outside of the TSP. - GovExec.com.

The G fund is self-contained. It is better viewed as a savings account rather than an investment fund. Like a savings account at a bank, the money in the account earns interest. While the rate of interest earned in the G fund varies, there is no risk to the money in the account.

The only "risk" is whether or not the interest rate of the G fund keeps up with the rate of inflation. If the G fund rate of return exceeds the inflation rate, investors are retaining purchasing power. If the rate is less than the inflation rate, investors are losing purchasing power.

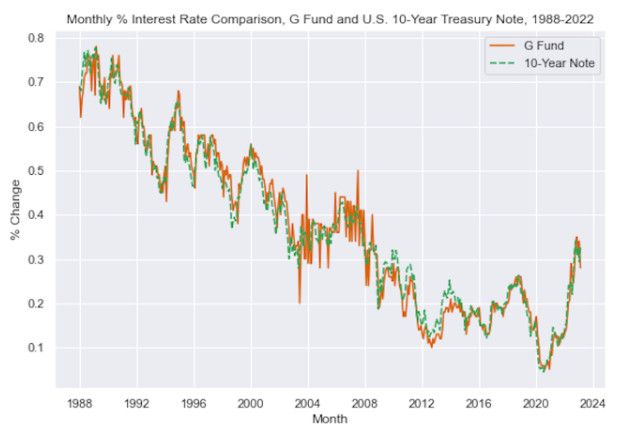

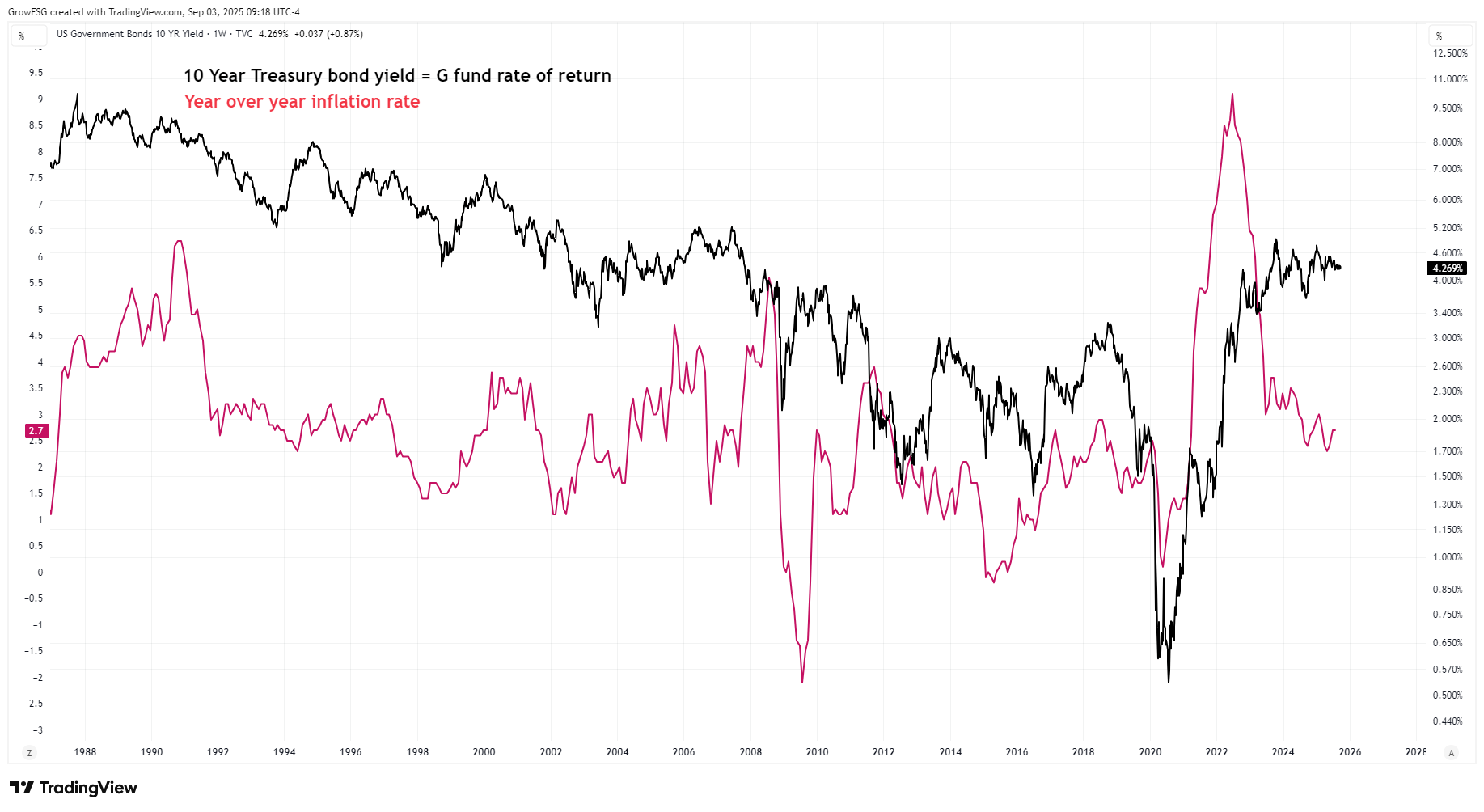

Many TSP investors point to the G fund "not keeping up with inflation". While there are times when this is true, it is generally not the case. The actual composition of the G fund is complicated, but its rate of return has correlated to the yield on the 10 year Treasury bond at over 98% as the chart from GovExec shows.

The chart below shows the 10 year bond yield, which generally equals the G fund rate of return, in black. The red line is the year over year inflation rate as reported by the Bureau of Labor and Statistics.

The scales on the chart are not equivalent but in general, when the black line is above the red line, the G fund rate of return is greater than the rate of inflation.

During a long-term bear market, the G fund is the most common choice for TSP investors. Because it acts as a savings account, there is no market risk. Because its rate of return is generally equivalent to the yield on the 10 year Treasury bond, it generally exceeds the rate of inflation. As such, the G fund is tough to beat when the stock funds are falling.

The Case For The F Fund

The F fund is a true bond fund. Unlike the G fund, there IS market risk associated with the F fund. According to TSP.gov, "The F Fund’s investment objective is to match the performance of the Bloomberg U.S. Aggregate Bond Index, a broad index representing the U.S. bond market.". The Aggregate Bond Index is traded under ticker symbol AGG. It's price fluctuates with the market.

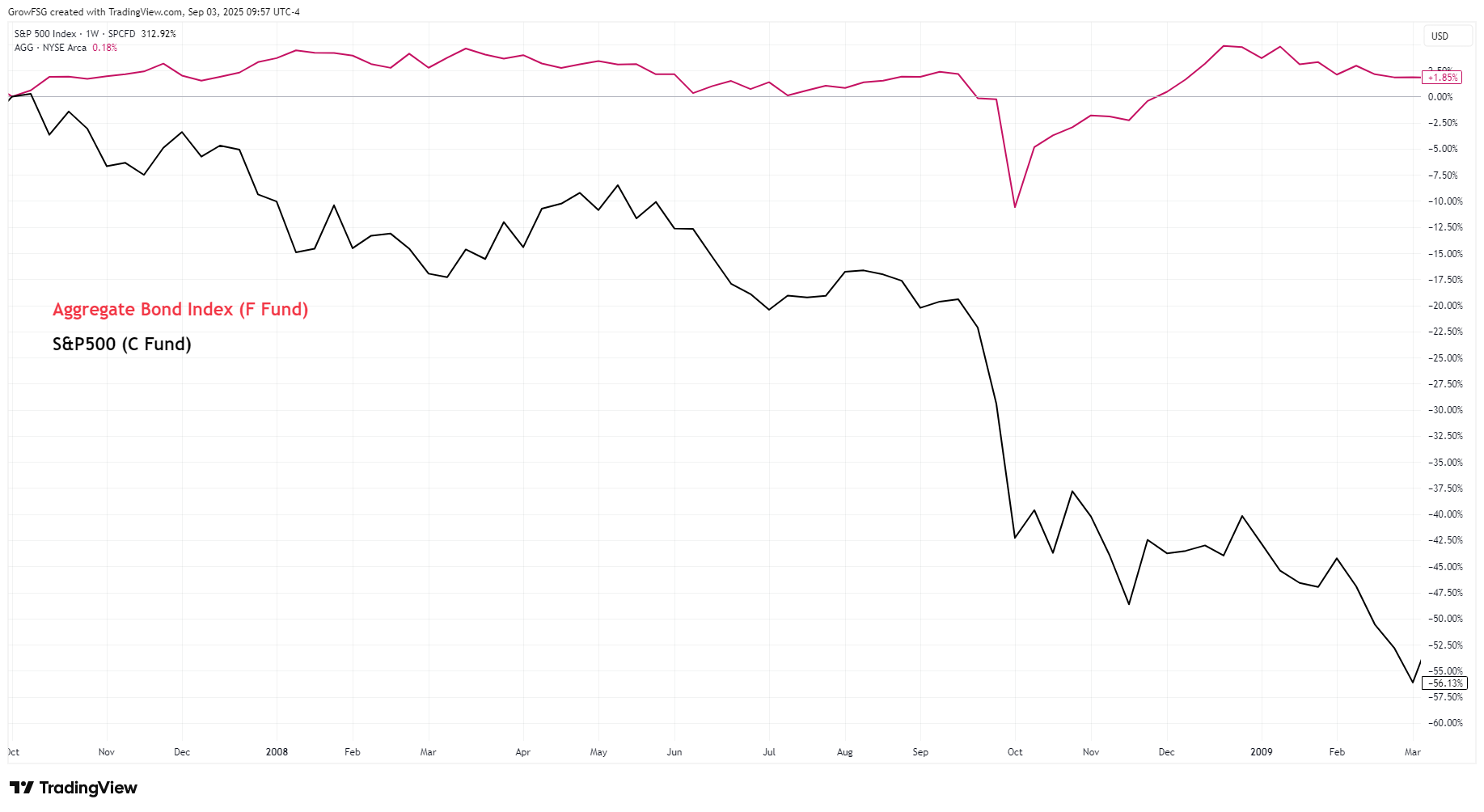

The last major bear market for the stock funds was the 2007-2009 Great Financial Crisis. From its peak in October 2007, the S&P500 (C fund) lost 56% of its value. Over that same period, the Aggregate Bond Index (F fund) gained almost 2%. The market risk of the F fund can be seen in the 10% decline during the last week of September 2008, but it was clearly a much better option for TSP investors versus the C fund throughout the Great Financial Crisis.

The Results

From early October 2007 through early March 2009, the C fund lost 56% of its value. Over that same time period, the G fund gained 5.3% and the F fund gained 1.85%. On its face, the G fund was the clear winner.

With no market risk and guaranteed gains equal to the rate of the 10 year Treasury bond, the G fund is hard to beat. Active traders can argue that more could have been made in the F fund but that is largely off-set by the guaranteed security of the G fund.

The bottom line is that either the G fund or the F fund were excellent choices for TSP investors during the last major bear market for stocks. Both protected investors from a 56% decline in the C fund, a 58% decline in the S fund, and a 63% decline in the I fund.

-----------------------------------------

GrowMyTSP.com does not provide personal investment advice. We are an education and analysis service, helping TSP investors grow their accounts using strategies and models that best fit their personal circumstances and risk tolerance. Get started at GrowMyTSP.com.